The Kwong Refund Window Is a Chance to Serve Your Clients (and Bill for It). The Deadline Is July 10.

There is a real, time-sensitive opportunity sitting in front of every tax preparer right now, and most of your clients have no idea it exists. A recent court decision could entitle millions of taxpayers to refunds of penalties and interest the IRS charged during the COVID years. The relief is not automatic. Someone has to identify it and claim it before July 10, 2026. That someone is you.

Here is what you need to know.

What changed

When the federal government declares a disaster, certain filing and payment deadlines are automatically postponed. The COVID-19 federal disaster ran for roughly three and a half years, from January 20, 2020 through May 11, 2023.

In Kwong v. United States, the U.S. Court of Federal Claims read IRC § 7508A to mean that filing and payment deadlines were postponed for that entire period, plus 60 days, through July 10, 2023. Under that reasoning, returns and payments that came due during the disaster period were not late, so the IRS should not have assessed failure-to-file penalties, failure-to-pay penalties, estimated tax penalties, or the related interest.

If that interpretation holds, a lot of your clients paid penalties and interest they never owed.

Who on your client list to look at

This is broad, not narrow. Your starting points:

- Clients who paid late-filing or late-payment penalties between January 20, 2020 and July 10, 2023

- Clients with penalties or interest assessed in that window but still unpaid (an abatement, not a refund)

- Clients who filed late international information returns, where penalties can be steep even with no tax due

- Non-filers for tax years 2019 through 2022 who had withholding or were owed refundable credits like the EITC, CTC, or Recovery Rebate Credit

- Clients who already filed but may benefit from an amended return claiming credits or deductions for those years

A practical first pass is to look at anyone who had a balance due on a 2019 through 2022 return, then pull transcripts from there. That filter is not perfect, since estimated tax penalties can hit clients who got refunds overall, but it gives you a prioritized queue instead of pulling transcripts blind across your whole book.

The deadlines

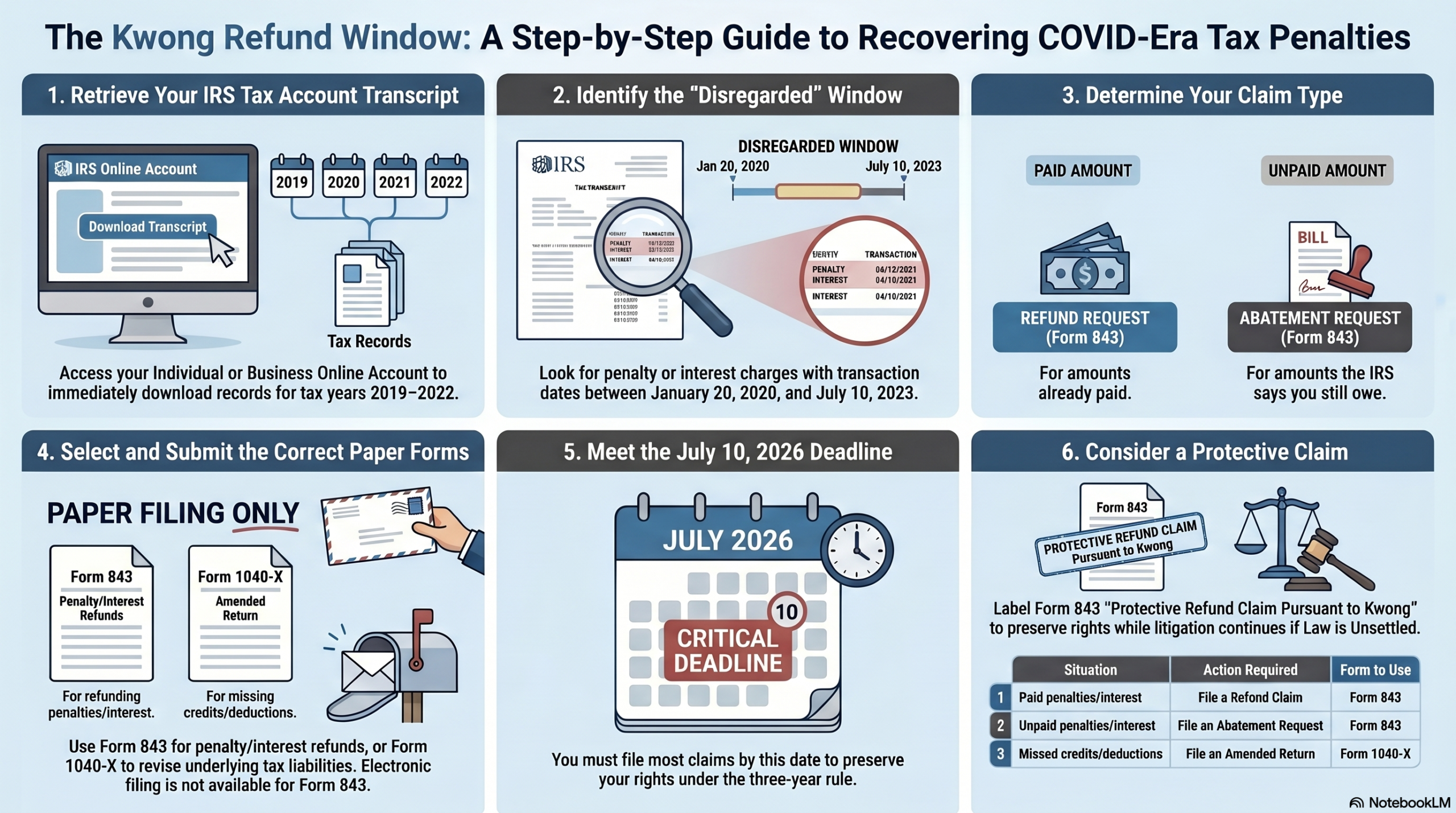

For most clients, the deadline is July 10, 2026, which is three years from the July 10, 2023 postponed due date. Two wrinkles worth knowing:

- If a client paid the penalties or interest after July 10, 2023, the two-years-from-payment rule may give them more time.

- Clients with open exams, active Appeals, or ongoing litigation may have additional time under open statutes. Evaluate those separately.

How to file

Start with the IRS account transcript. You are looking for penalty and interest transaction codes dated between January 20, 2020 and July 10, 2023.

From there:

- For penalties and interest already paid, file Form 843 as a refund claim.

- For amounts assessed but unpaid, file Form 843 as an abatement request. Different statute of limitations rules apply.

- If you cannot calculate the exact amount because the law is unsettled, file a protective claim. Write “Protective Refund Claim Pursuant to Kwong Case” across the top of Form 843, identify the tax year and the COVID-19 disaster issue, and include the dollar amount if known.

- To revise the underlying liability, use Form 1040-X. For non-filers, file the original return on paper.

A formal refund claim, where you can calculate the amount, has an advantage over a protective claim: if the IRS does not act within six months, it opens a path to federal court review. Protective claims sit in suspense until the issue resolves, which may take years.

Mechanics that trip people up: Form 843 is paper only, send it certified mail with return receipt, file a separate form for each tax period, and mail it to the service center for the client’s current Form 1040 filing address.

The honest caveat

The IRS disagrees with Kwong and an appeal is expected. This is unsettled law, and filing a claim does not guarantee a refund. But that uncertainty is the whole reason to act now. If your clients wait for a final ruling, the deadline to claim will almost certainly pass before that ruling arrives. Filing now is what preserves the right.

A caution worth passing along

The National Taxpayer Advocate has been explicit that scammers and aggressive promoters are already circling this issue, promising guaranteed refunds and charging fees based on refund size. That is a reputational risk for the whole profession. As a credentialed, ethical preparer, this is a moment to be the trusted voice for your clients, not to oversell. Explain the legal basis, set realistic expectations, and document your position.

The bottom line for your practice

This is billable work that genuinely helps clients, on a clear deadline, that almost none of them will ask for because they do not know to. Preparers who proactively review their 2019 through 2022 clients and file where warranted will protect real money for those clients and deepen the relationship in the process. The window closes July 10, 2026.

If you are a Tax Hound customer, we can give you a head start. As your service bureau we have access to your return data, and we can pull a list of your clients who had a balance due in tax years 2019 through 2022 so you are not pulling transcripts blind. It is not a complete picture, but it is a fast way to build your triage queue. Reply to our email on this, or reach out, and we will put it together for you.

This post is for general information and is not legal advice. For the full background, see the National Taxpayer Advocate’s four-part blog series on the Kwong issue at taxpayeradvocate.irs.gov.

{kind=link}